As filed with the Securities and Exchange Commission on June 21, 2021

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________

Form F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

________________________________

Arbe Robotics Ltd.

(Exact Name of Registrant as Specified in Its Charter)

________________________________

|

Israel |

7373 |

Not Applicable |

||

|

(State or Other Jurisdiction of |

(Primary Standard Industrial |

(I.R.S. Employer |

Arbe Robotics Ltd.

HaHashmonaim St. 107

Tel Aviv-Yafo

Israel

Telephone No.: +972-73-7969804, ext. 200

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

________________________________

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

(212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

________________________________

Copies to:

|

Richard I. Anslow, Esq. Asher S. Levitsky PC Ellenoff Grossman & Schole LLP 1345 Avenue of the Americas; Suite 1100 New York, New York 10105-0302 (212) 370-1300 |

Jon Venick, Esq. Jeremy Lustman, Esq. DLA Piper LLP (US) |

Shay Dayan, Adv.fMarf Lior Etgar, Adv. Erdinast, Ben Nathan, Toledano & Co. |

________________________________

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective and all other conditions to the business combination contemplated by the Business Combination Agreement described in the included proxy statement/prospectus have been satisfied or waived.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

|

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐ |

|

Exchange Act Rule 14d-1(d) (Cross-Border Third-party Tender Offer) ☐ |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

CALCULATION OF REGISTRATION FEE

|

Title of each Class of Security to be registered |

Amount to be Registered(1) |

Proposed |

Proposed |

Amount of |

|||||||

|

Ordinary Shares(4)(6) |

9,680,736 |

$ |

10.125(2) |

$ |

98,017,452.00 |

$ |

10,693.70 |

||||

|

Units, each consisting of one ordinary shares and one Warrant(3)(7) |

203,296 |

|

11.00 |

|

2,236,256.00 |

|

243.98 |

||||

|

Warrants(5)(7) |

10,729,500 |

|

1.105(2) |

|

11,856,097.50 |

|

1,293.50 |

||||

|

Ordinary Shares issuable on exercise of Warrants(6)(7) |

10,932,796 |

|

11.50(2) |

|

125,727,453.00 |

|

13,716.87 |

||||

|

Total |

|

$ |

237,837,258.50 |

$ |

25,948.05 |

||||||

____________

(1) All securities being registered will be issued by Arbe Robotics Ltd, a company organized under the laws of the State of Israel (“Arbe”), in connection with the Business Combination Agreement described in this registration statement (the “Business Combination Agreement”) and the proxy statement/prospectus included herein, which provides for, among other things, the merger of Autobot MergerSub, Inc., a Delaware corporation and wholly-owned subsidiary of Arbe (“Merger Sub”) with and into Industrial Tech Acquisitions, Inc., a Delaware corporation (“ITAC”), with ITAC surviving as a wholly-owned subsidiary of Arbe (the “Merger”). As a result of the Merger (and following a pre-closing reorganization of Arbe), (i) each outstanding share of Class A common stock, par value $0.0001 per share and each outstanding shares of Class B common stock, par value $.0001 per share, of ITAC (collectively, the “ITAC Common Stock”) will be converted into the right to receive one Arbe Ordinary Share (“Arbe Ordinary Share”), and (ii) to purchase shares of ITAC Common Stock (the “ITAC Warrants”) outstanding at the Effective Time will be converted into the right to receive a warrant (the “Arbe Warrants”) to purchase an equal number of Arbe Ordinary Shares at the same exercise price of $11.50 per share.

(2) In accordance with Rule 457(f)(1) and Rule 457(c), as applicable, based on (i) in respect of Arbe Ordinary Shares issued to ITAC security holders, the average of the high ($10.18) and low ($10.07) prices of the ITAC Class A Common Stock on the Nasdaq Stock Market (“Nasdaq”) on June 16, 2021, (ii) in respect of Arbe Warrants issued to ITAC security holders, the average of the high ($1.17) and low ($1.04) prices for the ITAC Warrants on Nasdaq on June 16, 2021 and (iii) in respect of Arbe Ordinary Shares issuable upon exercise of the Arbe Warrants the exercise price of the Arbe ($11.50 per share).

(3) Represents units issuable pursuant to the Underwriter’s Warrants pursuant to which the underwriter of ITAC’s initial public offering has the right to purchase units at a price of $11.00 per unit.

(4) Represents Arbe Ordinary Shares issuable in exchange for outstanding ITAC Common Stock pursuant to the Merger.

(5) Represents Arbe Warrants, each Arbe Warrant entitling the holder to purchase one Arbe Ordinary Share, issuable in exchange for ITAC Warrants pursuant to the Merger.

(6) Represents Arbe Ordinary Shares issuable upon exercise of the Arbe Warrants, including Arbe Warrants issuable upon exercise of the underwriter’s warrant.

(7) Pursuant to Rule 416(a), there are also being registered an indeterminable number of additional securities as may be issued to prevent dilution resulting from share splits, share dividends or similar transactions.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this proxy statement/prospectus is not complete and may be changed. We may not issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

|

PRELIMINARY PROSPECTUS |

SUBJECT TO COMPLETION, DATED JUNE 21, 2021 |

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS

OF

INDUSTRIAL TECH ACQUISITIONS, INC.

and

PROSPECTUS FOR UP TO 9,680,736 ORDINARY SHARES, 10,932,796 WARRANTS AND 10,932,796

ORDINARY SHARES ISSUABLE UPON EXERCISE OF WARRANTS

OF

ARBE ROBOTICS LTD.

The board of directors of Industrial Tech Acquisitions, Inc., a Delaware corporation (“ITAC”), unanimously approved entry by ITAC into the Business Combination Agreement dated as of March 18, 2021 (the “Business Combination Agreement”), by and among Arbe Robotics Ltd., an Israeli company (“Arbe”), Autobot MergerSub, Inc., a Delaware corporation and wholly-owned subsidiary of Arbe (“Merger Sub”), and ITAC, which provides for, among other things and subject to the terms and conditions set forth therein, the merger of Merger Sub with and into ITAC, with ITAC surviving as a wholly-owned subsidiary of Arbe, as a result of which (i) the holders of ITAC’s Class A Common Stock and Class B Common Stock (collectively, ITAC Common Stock”) becoming holders of an equal number of ordinary shares of Arbe (“Arbe Ordinary Shares”), and (ii) the holders of outstanding warrants to purchase shares of ITAC Common Stock (“ITAC Warrants”) becoming warrants (“Arbe Warrants”) to purchase an equal number of Arbe Ordinary Shares at the same exercise price per Arbe Ordinary Share and for the same exercise period. The Merger and the other transactions contemplated by the Business Combination Agreement, are collectively referred to herein as the “Merger.”

Pursuant to the Business Combination Agreement, immediately prior to the effective time of the Merger (the “Effective Time”), and contingent upon the Closing, Arbe will effect a recapitalization (the “Recapitalization”) pursuant to which (a) each outstanding warrant (collectively, the “Outstanding Arbe Warrants”) to purchase Arbe Ordinary Shares or Arbe Preferred Shares (other than any Outstanding Arbe Warrants which (1) are not required by their terms to be exercised in connection with the Transactions, and (2) are not exercised at the election of the holder thereof prior to the consummation of the Recapitalization, all of which unexercised warrants being referred to as the “Continuing Warrants”) will be exercised in accordance with their respective terms (all such Outstanding Company Warrants so exercised, the “Exercising Arbe Warrants”), (b) immediately following such exercise, each outstanding Arbe Preferred Share will become and be converted into Arbe Ordinary Shares in accordance with Arbe’s Amended and Restated Company Articles of Association currently in effect (the “Existing Arbe Articles”) and (c) immediately following such conversion, but for the avoidance of doubt prior to the Effective Time, each then outstanding Arbe Ordinary Share shall, as a result of the Recapitalization, be converted into such number Arbe Ordinary Shares as is determined by multiplying (1) such Arbe Ordinary Share by (2) the quotient obtained by dividing (A) the sum of (i) $525,000,000, plus (ii) on a dollar-for-dollar basis equal to the amount by which the ITAC Transaction Expenses (other than expenses relating to the PIPE Investment) (in each instance, as defined in the Business Combination Agreement) exceed $7.0 million, by (B) $10.00, and subsequently dividing such quotient by (C) the sum of (i) the number of Arbe Ordinary Shares outstanding and (ii) without duplication, the number of Arbe Ordinary Shares issuable upon the exercise of all then outstanding (x) Continuing Warrants and (y) options to purchase shares of Arbe Ordinary Shares (including, any options granted subsequent to the date of the Business Combination Agreement (collectively, the “Outstanding Company Options,” but excluding, in each instance, for the avoidance of doubt, any Arbe Ordinary Shares issued or issuable in connection with the PIPE Investment), and taking such quotient to five decimal places, which ratio is referred to as the “Conversion Ratio.”

The registration statement of which this proxy statement/prospectus is a part covers the Arbe Ordinary Shares and Arbe Warrants issuable to the stockholders and warrant holders of ITAC as described above, excluding any shares of ITAC Common Stock issued to the PIPE Investors at the closing of the Merger, any shares of ITAC Common Stock with respect to which public holders exercised their right of redemption under ITAC’s certificate of incorporation, as currently in effect, and any Arbe Ordinary Shares held prior to the consummation of the Merger by shareholders of Arbe. Accordingly, we are registering up to an aggregate of 20,823,008 Arbe Ordinary Shares, which represents 9,680,736 Arbe Ordinary Shares issued with respect to the outstanding ITAC Common Stock and 11,142,272 Arbe Ordinary Shares issuable upon the exercise of the Arbe Warrants, including Arbe Warrants issuable upon exercise

of the underwriter’s unit purchase option, and 10,932,796 Arbe Warrants, including Arbe Warrants issuable upon exercise of the underwriter’s unit purchase option. These numbers assume that no ITAC public stockholders exercise their redemption right. We are not registering with this registration statement the Arbe Ordinary Shares issuable to the PIPE Investors or any Arbe Ordinary Shares held prior to the consummation of the Merger by stockholders of Arbe.

Proposals to approve the Business Combination Agreement and the other matters discussed in this proxy statement/prospectus will be presented at the Special Meeting of ITAC stockholders scheduled to be held on , 2021 in virtual format.

Although Arbe is not currently a public reporting company, following the effectiveness of the registration statement of which this proxy statement/prospectus is a part and the closing of the Merger, Arbe will become subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Arbe intends to apply for listing of the Arbe Ordinary Shares and Arbe Warrants on Nasdaq under the proposed symbols “ARBE” and “ARBEW,” respectively, to be effective at the consummation of the Merger. It is a condition of the consummation of the Merger that the Arbe Ordinary Shares are approved for listing on Nasdaq (subject only to official notice of issuance thereof). While trading on Nasdaq is expected to begin on the first business day following the date of completion of the Merger, there can be no assurance that Arbe’s securities will be listed on Nasdaq or that a viable and active trading market will develop following the consummation of the Merger. See “Risk Factors” beginning on page 38 for more information.

Effective as of closing, Arbe will be an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, and is therefore eligible to take advantage of certain reduced reporting requirements otherwise applicable to other public companies.

Effective as of closing, it is expected that Arbe will qualify as a “foreign private issuer” as defined in the Exchange Act and will therefore be exempt from certain rules under the Exchange Act that impose certain disclosure obligations and procedural requirements for proxy solicitations under Section 14 of the Exchange Act. In addition, in connection with such status, Arbe’s officers, directors and principal shareholders would be exempt from the reporting and “short-swing” profit recovery provisions under Section 16 of the Exchange Act. Moreover, Arbe would not be required to file periodic reports and financial statements with the U.S. Securities and Exchange Commission as frequently or as promptly as U.S. domestic registrants whose securities are registered under the Exchange Act.

The accompanying proxy statement/prospectus provides ITAC stockholders with detailed information about the Merger and other matters to be considered at the Special Meeting of ITAC. We encourage you to read the entire accompanying proxy statement/prospectus, including the Annexes and other documents referred to therein, carefully and in their entirety. You should also carefully consider the risk factors described in “Risk Factors” beginning on page 38 of the accompanying proxy statement/prospectus.

None of the Securities and Exchange Commission or any state securities commission has approved or disapproved of the securities to be issued in connection with the Merger, or determined if this proxy statement/prospectus is accurate or adequate. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated , 2021, and is first being mailed to ITAC stockholders on or about , 2021.

|

ALL HOLDERS (THE “PUBLIC STOCKHOLDERS”) OF CLASS A SHARES ISSUED IN ITAC’S INITIAL PUBLIC OFFERING (THE “PUBLIC SHARES”) HAVE THE RIGHT TO HAVE THEIR PUBLIC SHARES REDEEMED FOR CASH IN CONNECTION WITH THE PROPOSED BUSINESS COMBINATION. PUBLIC STOCKHOLDERS ARE NOT REQUIRED TO AFFIRMATIVELY VOTE FOR OR AGAINST THE BUSINESS COMBINATION PROPOSAL, TO VOTE ON THE BUSINESS COMBINATION PROPOSAL AT ALL, OR TO BE HOLDERS OF RECORD ON THE RECORD DATE IN ORDER TO HAVE THEIR SHARES REDEEMED FOR CASH. THIS MEANS THAT ANY PUBLIC STOCKHOLDER HOLDING PUBLIC SHARES MAY EXERCISE REDEMPTION RIGHTS REGARDLESS OF WHETHER THEY ARE EVEN ENTITLED TO VOTE ON THE BUSINESS COMBINATION PROPOSAL. TO EXERCISE REDEMPTION RIGHTS, SEE “REDEMPTION RIGHTS” FOR MORE SPECIFIC INSTRUCTIONS. |

INDUSTRIAL TECH ACQUISITONS, INC.

5090 Richmond Avenue, Suite 319

Houston, TX 77056

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2021

TO THE STOCKHOLDERS OF INDUSTRIAL TECH ACQUISITONS, INC.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders of Industrial Tech Acquisitions, Inc., a Delaware corporation (“ITAC”), will be held virtually at Eastern time, on , 2021, accessible at or at such other time, on such other date and at such other place to which the meeting may be adjourned or postponed (the “Special Meeting”). You are cordially invited to attend the Special Meeting, which will be held for the following purposes:

(1) to consider and vote upon a proposal to adopt the Business Combination Agreement dated as of March 18, 2021 (the “Business Combination Agreement”), by and among Arbe Robotics Ltd., an Israeli company (“Arbe”), Autobot MergerSub, Inc., a Delaware corporation and wholly-owned subsidiary of Arbe (“Merger Sub”), and ITAC, which provides for, among other things, (A) the merger (the “Merger”) of Merger Sub with and into ITAC, with ITAC surviving as a wholly-owned subsidiary of Arbe, and (B) in connection therewith (1) the holders of ITAC’s Class A Common Stock and Class B Common Stock (collectively, “ITAC Common Stock”) becoming holders of an equal number of ordinary shares of Arbe (“Arbe Ordinary Shares”), and (2) the holders of Warrants to purchase shares of ITAC Common Stock (“ITAC Warrants”) becoming holders of warrants (“Arbe Warrants”) to purchase an equal number of Arbe Ordinary Shares at the same exercise price per share and for the same exercise period (the Merger and the other transactions contemplated by the Business Combination Agreement, the “Transactions”);

(2) to consider and vote upon a proposal to amend, immediately following and in connection with the closing of the Merger, ITAC’s existing amended and restated certificate of incorporation (the “Existing ITAC Charter”) by adopting the second amended and restated certificate of incorporation attached hereto as Annex C (the “Restated ITAC Charter”), which we refer to as the “ITAC Charter Proposal”; and

(3) to consider and vote upon a proposal to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the Special Meeting, ITAC is not authorized to consummate the Merger or adopt the ITAC Charter Proposal, which we refer to as the “Adjournment Proposal.”

These items of business are described in the attached proxy statement/prospectus, which we encourage you to read in its entirety before voting. Only holders of record of ITAC Common Stock at the close of business on , 2021, are entitled to notice of the Special Meeting and to vote and have their votes counted at the Special Meeting and any adjournments or postponements of the Special Meeting.

After careful consideration, the ITAC board of directors has determined that each of (i) the Business Combination Proposal, (ii) the ITAC Charter Proposal and (iii) the Adjournment Proposal are advisable and fair to and in the best interest of ITAC and its stockholders and unanimously recommends that you vote or give instruction to vote “FOR” the Business Combination Proposal, “FOR” the ITAC Charter Proposal, and “FOR” the Adjournment Proposal, if presented.

The Merger is conditioned on the approval of each of the Business Combination Proposal and the ITAC Charter Proposal (the “Condition Precedent Proposals”) at the Special Meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of the other. The Adjournment Proposal is not conditioned upon the approval of any other proposal. Each of these proposals is more fully described in the accompanying proxy statement/prospectus, which each stockholder is encouraged to read carefully and in its entirety. If the Business Combination Proposal is not approved by ITAC’s stockholders, the Merger will not be consummated and the Restated ITAC Charter will not be adopted.

All of ITAC’s stockholders are cordially invited to attend the Special Meeting virtually. To ensure your representation at the Special Meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If you are a stockholder of record of ITAC Common Stock, you may also cast your vote virtually at the

Special Meeting. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares or, if you wish to attend the Special Meeting and vote in person, you must obtain a proxy from your broker or bank. If you do not vote or do not instruct your broker or bank how to vote, it will have the same effect as voting against the Business Combination Proposal and the ITAC Charter Proposal, but will have no effect on the Adjournment Proposal.

A complete list of ITAC stockholders of record entitled to vote at the Special Meeting will be available for ten days immediately prior to the Special Meeting at the principal executive offices of ITAC for inspection by stockholders during ordinary business hours for any purpose germane to the Special Meeting.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the Special Meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker or bank to ensure that votes related to the shares you beneficially own are properly counted. The Merger is conditioned on the approval of each of the Condition Precedent Proposals at the Special Meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of the other. The Adjournment Proposal is not conditioned upon the approval of any other proposal. Each of the proposals is more fully described in the accompanying proxy statement/prospectus, which each ITAC stockholder is encouraged to read carefully and in its entirety.

Thank you for your participation. We look forward to your continued support.

This proxy statement/prospectus is dated , 2021 and is first being mailed to ITAC stockholders on or about , 2021.

By Order of the Board of Directors

|

/s/ E. Scott Crist |

||

|

E. Scott Crist |

||

|

Chief Executive Officer and Chairman of the Board |

Houston, Texas

, 2021

|

Page |

||

|

1 |

||

|

1 |

||

|

1 |

||

|

1 |

||

|

2 |

||

|

7 |

||

|

10 |

||

|

22 |

||

|

Historical Comparative and Pro Forma Combined Per Share Data of ITAC and Arbe |

36 |

|

|

37 |

||

|

38 |

||

|

79 |

||

|

81 |

||

|

84 |

||

|

106 |

||

|

108 |

||

|

109 |

||

|

110 |

||

|

Agreements Entered into in Connection with the Merger Agreement |

115 |

|

|

118 |

||

|

134 |

||

|

140 |

||

|

148 |

||

|

ITAC’S Management’s Discussion and Analysis of Financial Condition and Results of Operations |

149 |

|

|

153 |

||

|

167 |

||

|

172 |

||

|

176 |

||

|

Arbe’s Management’s Discussion and Analysis of Finaincial Condition and Results of Operations |

177 |

|

|

Unaudited Pro Forma Condensed Combined Financial Information |

186 |

|

|

198 |

||

|

209 |

||

|

213 |

||

|

221 |

||

|

225 |

||

|

232 |

||

|

232 |

||

|

232 |

||

|

233 |

||

|

233 |

||

|

F-1 |

|

ANNEXES |

||

|

A-1 |

||

|

Annex B: Restated Arbe Articles |

B-1 |

|

|

Annex C: Restated ITAC Charter |

C-1 |

i

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This proxy statement/prospectus, which forms part of a registration statement on Form F-4 filed with the U.S. Securities and Exchange Commission (the “SEC”) by Arbe, constitutes a prospectus of Arbe under Section 5 of the U.S. Securities Act of 1933, as amended (the “Securities Act”), with respect to (i) the Arbe Ordinary Shares to be issued to ITAC stockholders in connection with the consummation of the Merger, (ii) the Arbe Warrants to be issued to holders of ITAC Warrants in connection with the consummation of the Merger, and (iii) the Arbe Ordinary Shares underlying the Arbe Warrants, in each instance, if the Merger is consummated. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the U.S. Securities Exchange Act of 1934, as amended, with respect to the Special Meeting of ITAC stockholders at which ITAC stockholders will be asked to consider and vote upon a proposal to approve the Merger by the adoption of the Business Combination Agreement and the ITAC Charter Proposal, among other matters.

Unless otherwise indicated or the context otherwise requires, all references in this proxy statement/prospectus to the terms “Arbe” and the “Company” refer to Arbe Robotics Ltd., together with its subsidiaries. All references in this proxy statement/prospectus to “ITAC” refer to Industrial Tech Acquisitions, Inc.

Information in this proxy statement/prospectus relating to the number of outstanding Arbe Ordinary Shares and per share information, unless otherwise provided, reflect the present capitalization of Arbe. As a result of the Recapitalization described in this proxy statement/prospectus, the number of outstanding Arbe Ordinary Shares will change which will result in a change in the per share information.

Certain amounts described herein have been expressed in U.S. dollars for convenience and, when expressed in U.S. dollars in the future, such amounts may be different from those set forth herein due to intervening exchange rate fluctuations.

In this proxy statement/prospectus, we present industry data, information and statistics regarding the markets in which Arbe competes as well as publicly available information, industry and general publications and research and studies conducted by third parties. This information is supplemented where necessary with Arbe’s own internal estimates, taking into account publicly available information about other industry participants and Arbe’s management’s judgment where information is not publicly available. This information appears in “Summary of the Proxy Statement/Prospectus,” “Arbe’s Management’s Discussion and Analysis of Financial Condition and Results of Operation,” “Information About the Companies — Arbe’s Business” and other sections of this proxy statement/prospectus.

Industry publications, research, studies and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this proxy statement/prospectus. These forecasts and forward-looking information are subject to uncertainty and risk due to a variety of factors, including those described under “Risk Factors.” These and other factors could cause results to differ materially from those expressed in any forecasts or estimates.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

ITAC and Arbe own or have rights to trademarks, trade names and service marks that they use in connection with the operation of their businesses. In addition, their names, logos and website names and addresses are their trademarks or service marks. Other trademarks, trade names and service marks appearing in this proxy statement/prospectus are the property of their respective owners. Solely for convenience, in some cases, the trademarks, trade names and service marks referred to in this proxy statement/prospectus are listed without the applicable “©,” “SM” and “TM” symbols, but they will assert, to the fullest extent under applicable law, their rights to these trademarks, trade names and service marks.

1

Unless otherwise stated or unless the context otherwise requires, the terms “Arbe” and the “Company” refer to Arbe Robotics Ltd., a company organized under the laws of Israel, the term “ITAC” refers to Industrial Tech Acquisitions, Inc., a Delaware corporation, and “Merger Sub” refers to Autobot MergerSub, Inc., a Delaware corporation and a direct, wholly-owned subsidiary of Arbe.

In addition, in this proxy statement/prospectus:

“2021 Plan” means the new equity incentive plan for Arbe pursuant to which Arbe may grant equity-based incentive awards to attract, motivate and retain the talent for which it competes, such plan to be in substantially the form filed as an exhibit to the registration statement of which this proxy statement/prospectus is a part.

“Adjournment Proposal” means the proposal to adjourn the Special Meeting of the stockholders of ITAC to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the Special Meeting, there are not sufficient votes to approve the Business Combination Proposal or the ITAC Charter Proposal.

“Arbe Lock-up Agreement” means the agreements dated as of March 18, 2021 pursuant to which certain of Arbe’s principal shareholders agreed not to sell Arbe shares, subject to specified release provisions, during the one-year period commencing on the Closing Date.

“Arbe Ordinary Shares” means Arbe’s ordinary shares, with a nominal value of NIS 0.01 per share, having one vote per share; provided, however, that, as a result of, and in connection with, the Recapitalization, the nominal value of the Arbe Ordinary Share will be NIS 0.000216 per share.

“Arbe Preferred Shares” means the preferred shares, with a nominal value of NIS 0.01 per share, of Arbe, which will be converted into Arbe Ordinary Shares pursuant to the Recapitalization prior to the Effective Time.

“Arbe Shareholder Approval Matters” means (i) the adoption and approval of the Business Combination Agreement and the Transactions; (ii) the approval of the Restated Arbe Articles and the Recapitalization; (iii) the adoption and approval of the 2021 Plan; (iv) the appointment of the members of the Post-Closing Board of Directors of Arbe; (v) the issuance of Arbe Ordinary Shares and Arbe Warrants pursuant to the Business Combination Agreement, including (x) the Arbe Ordinary Shares issuable in connection with the PIPE Investment, (y) the Arbe Ordinary Shares issuable pursuant to the Recapitalization, and (z) the Arbe Ordinary Shares issuable upon exercise of the Arbe Warrants, the Continuing Arbe Warrants and Outstanding Arbe Options; and (vi) such other matters as Arbe and ITAC may mutually determine to be necessary or appropriate in order to effect the Transactions.

“Arbe Warrants” means the warrants to purchase Arbe Ordinary Shares to be issued to the holders of ITAC Warrants in connection with the consummation of the Merger.

“Broker Non-Vote” means the failure of an ITAC stockholder who holds shares in “street name” through a broker or other nominee, to give voting instructions to such broker or other nominee.

“Business Combination Agreement” means the Business Combination Agreement, dated as of March 18, 2021, by and among ITAC, Arbe and Merger Sub, as such agreement may be amended or otherwise modified from time to time in accordance with its terms.

“Business Combination Proposal” means the proposal to adopt the Business Combination Agreement and approve the Transactions contemplated thereby.

“Closing” shall mean the closing of the Merger.

“Continuing Arbe Warrants” means Outstanding Arbe Warrants which (1) are not required by their terms to be exercised in connection with the Merger and (2) are not exercised at the election of the holder thereof prior to the consummation of the Recapitalization.

“Conversion Ratio” means such number Arbe Ordinary Shares as is determined by multiplying (1) one Arbe Ordinary Share by (2) the quotient obtained by dividing (A) the sum of (i) $525,000,000, plus (ii) on a dollar-for-dollar basis equal to the amount, if any, by which the ITAC Transaction Expenses (other than expenses relating to the PIPE Investment) (as defined in the Business Combination Agreement) exceed $7,000,000, by (B) $10.00, and subsequently dividing

2

such quotient by (C) the sum of (i) the number of Arbe Ordinary Shares then outstanding and (ii) without duplication, the number of Arbe Ordinary Shares issuable upon the exercise of all then outstanding Continuing Arbe Warrants and Outstanding Arbe Options, (but excluding, in each instance, for the avoidance of doubt, any Arbe Ordinary Shares issued or issuable in connection with the PIPE Investment), and taking such quotient to five decimal places.

“Deadline Date” means the date by which ITAC must complete a business combination failing which it is required to liquidate, with the Trust Account being paid over to the holders of the Public Shares. Such date is December 11, 2021, which date may be extended for up to two periods of three months each upon payment into the Trust Account of an extension payment of $763,260 for each such three-month extension.

“DGCL” means the Delaware General Corporation Law.

“DTC” means The Depository Trust Company.

“Effective Time” means the effective time of the Merger pursuant to the Business Combination Agreement.

“Enhanced Lock-up Restrictions” means the additional restrictions to which the Sponsor is subject pursuant to the Founder Lock-Up Agreement.

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“Exercising Arbe Warrants” means Outstanding Arbe Warrants, other than the Continuing Arbe Warrants, which have been exercised prior to or as a part of the Recapitalization.

“Existing Arbe Articles” means the Amended and Restated Articles of Association of Arbe in effect on the date of this proxy statement/prospectus.

“Existing ITAC Charter” means ITAC’s amended and restated certificate of incorporation as in effect on the date of this proxy statement/prospectus.

“Founder Lock-up Agreement” means the lock-up agreement, dated March 18, 2021, pursuant to which the Sponsor agreed to certain restrictions on the sale of the Arbe Ordinary Shares to be issued to the Sponsor pursuant to the Business Combination Agreement in addition to the restrictions set forth in the Letter Agreement.

“Founder Registration Rights Agreement” means the registration rights agreement, dated as of September 8, 2020, pursuant to which ITAC granted registration rights to the Sponsor.

“Founder Registration Rights Agreement Amendment” means the first amendment dated March 18, 2021 to the Founder Registration Rights Agreement pursuant to which Arbe agreed to assume the obligations of ITAC under the Founder Registration Rights Agreement.

“Founder Shares” means the shares of ITAC Class B Common Stock initially purchased by the Sponsor in a private placement prior to the IPO.

“Insiders” means the executive officers and directors of ITAC.

“IPO” means the initial public offering of Units of ITAC, pursuant to its prospectus dated September 8, 2020.

“Israeli Companies Law” means the Israeli Companies Law, 5759-1999, as amended.

“ITAC Charter Proposal” means the proposal to amend and restate the Existing ITAC Charter to change the corporate name of ITAC to Autobot HoldCo, Inc., to change the authorized capital stock to 100 shares of common stock and to otherwise restate the Existing ITAC Charter to a certificate of incorporation appropriate for a privately owned corporation, such amendment and restatement to become effective upon the effectiveness of the Merger.

“ITAC Class A Common Stock” means ITAC’s Class A common stock, par value $0.0001 per share.

“ITAC Class B Common Stock” means ITAC’s Class B common stock, par value $0.0001 per share.

“ITAC Common Stock” means ITAC Class A Common Stock and ITAC Class B Common Stock.

3

“ITAC Private Warrants” means the ITAC Warrants sold to the Sponsor in a private placement in connection with the IPO or otherwise sold in a private placement and include any ITAC Warrants issued upon conversion of any convertible promissory note issued to the Sponsor.

“ITAC Public Warrants” means ITAC Warrants included in Units sold in the IPO.

“ITAC Warrant” means a warrant to purchase one share of ITAC Class A Common Stock at a price of $11.50 per share, which may be either an ITAC Public Warrant or an ITAC Private Warrant.

“Letter Agreement” means the Letter Agreement, by and between ITAC, its officers and directors and the Sponsor, pursuant to which the Sponsor and ITAC’s officers and directors agreed, among other things, to vote in favor of any proposed business combination, not to seek any redemption of any shares of ITAC Common Stock owned by them, and to certain lock-up provisions.

“Maxim” means Maxim Group LLC, the underwriter of ITAC’s IPO.

“Maximum Redemption Scenario” assumes that that all Public Stockholders holding 7,623,600 Public Shares will exercise their redemption rights for the approximately $77.0 million of funds in the Trust Account. Arbe’s obligations under the Business Combination Agreement are subject, among other conditions, to the amount of cash and cash equivalents of ITAC at the Closing, including cash not redeemed from the Trust Account and cash raised in the PIPE Investment (which, for the avoidance of doubt, solely for purposes of the computation of Minimum Cash Requirement includes any cash paid to Arbe if Arbe exercises its right to directly issue Arbe Ordinary Shares pursuant to the PIPE Subscription Agreements) will not be less than $100,000,000 (after giving effect to redemptions of ITAC’s public stockholders, but prior to the payment of ITAC’s or Arbe’s Transaction Expenses or other liabilities due at the Closing (the “Minimum Cash Condition”). Under the Existing ITAC Charter, ITAC is prohibited from redeeming or repurchasing Public Shares submitted for redemption if such redemption would result in ITAC’s or Arbe’s failure to have net tangible assets (as determined in accordance with Rule3a5l-l(g)(1) of the Exchange Act (or any successor rule)) in excess of $5,000,001. As ITAC expects that, at Closing, ITAC or Arbe will retain at least the minimum required capital to satisfy ITAC’s obligation to maintain net tangible assets in excess of $5,000,001, the Minimum Cash Condition will be satisfied if the PIPE investors consummate their PIPE investments for an aggregate of $100 million of Arbe Ordinary Shares.

“Merger” means the merger of Merger Sub with and into ITAC, with ITAC surviving the merger and becoming a wholly-owned subsidiary of Arbe, along with the other transactions contemplated by the Business Combination Agreement.

“Minimum Cash Requirement” means that the aggregate amount of cash and cash equivalents of ITAC at the Closing, including cash not redeemed from the Trust Account and cash raised in the PIPE Investment (which, for the avoidance of doubt, solely for purposes of the computation of Minimum Cash Requirement includes any cash paid to Arbe if Arbe exercises its right to directly issue Arbe Ordinary Shares pursuant to the Subscription Agreements with the PIPE Investors) will not be less than $100,000,000 (after giving effect to redemptions of ITAC’s public stockholders, but prior to the payment of ITAC’s or Arbe’s Transaction Expenses or other liabilities due at the Closing).

“Nasdaq” means the Nasdaq Stock Market.

“No Redemption Scenario” means a scenario in which no Public Stockholder elects to have his or her Public Shares redeemed in connection with the Merger.

“Outstanding Arbe Options” means outstanding options to purchase Arbe Ordinary Shares issued pursuant to Arbe’s existing option plans that are outstanding on the date of the Recapitalization.

“Outstanding Arbe Warrants” means the warrants issued by Arbe which are outstanding on the date of the Business Combination Agreement which give the holders the right to purchase Arbe Ordinary Shares or Arbe Preferred Shares, as applicable.

“PIPE Investment” means the purchases of PIPE Shares pursuant to PIPE Subscription Agreements with the PIPE Investors, such purchases to be consummated immediately prior to the consummation of the Merger.

“PIPE Investors” means certain accredited investors who executed PIPE Subscription Agreements pursuant to which they agreed, in the aggregate, to purchase the PIPE Shares.

4

“PIPE Shares” means 10,000,000 shares of ITAC Class A Common Stock subscribed for and to be purchased by the PIPE Investors pursuant to the PIPE Subscription Agreements; provided, however, that in lieu of such shares of ITAC Class A Common Stock, Arbe has the right to issue Arbe Ordinary Shares to the PIPE Investors upon completion of the Recapitalization (with the PIPE Shares not participating in the Recapitalization) in the same number and the same price per share that would apply if ITAC were the issuer.

“PIPE Subscription Agreements” means the subscription agreements entered into by the PIPE Investors, pursuant to which the PIPE Investors have committed to subscribe for and purchase the PIPE Shares at a purchase price per share of $10.00.

“Post-Closing Board of Directors” means the board of directors of Arbe composed of seven directors, consisting of four directors designated by Arbe, at least two of whom will be considered independent under Nasdaq requirements; one director designated by ITAC, and two independent directors (under Nasdaq requirements) mutually agreed upon by Arbe and ITAC.

“Prospectus” means the prospectus dated September 8, 2020 included in the Registration Statements on Form S-1 (Registration No. 333-242339) filed by ITAC with the SEC in connection with the IPO.

“Public Shares” means shares of ITAC Class A Common Stock issued as part of the Units sold in the IPO.

“Public Stockholders” means the holders of Public Shares of ITAC.

“Recapitalization” means the recapitalization whereby (i) all Exercising Arbe Warrants are exercised in accordance with their terms, (ii) all outstanding Arbe Preferred Shares are converted into Arbe Ordinary Shares in accordance with their terms and the Existing Arbe Charter, and (iii) each Arbe Ordinary Share that is outstanding after the exercise and conversion pursuant to clauses (i) and (ii) of this definition will become and be converted into such number of Arbe Ordinary Shares as is determined by multiplying such Arbe Ordinary Share by the Conversion Ratio. Each Outstanding Arbe Warrant and Outstanding Arbe Option shall be adjusted to reflect the Recapitalization.

“Redemption” means ITAC’s acquisition of Public Shares in connection with the Merger pursuant to the right of the holders of Public Shares to have their shares redeemed in accordance with the procedures described in this proxy statement/prospectus.

“Restated Arbe Articles” means the amendment and restatement of the Existing Arbe Articles, in the form attached to this proxy statement/prospectus as Annex B, and approved by the Arbe shareholders as one of the Arbe Shareholder Approval Matters.

“Restated ITAC Charter” means the amended and restated certificate of incorporation of ITAC in the form attached as Annex C to this proxy statement/prospectus which changes the corporate name of ITAC to Autobot HoldCo, Inc., changes the authorized capital stock of ITAC to 100 shares of common stock and otherwise restates the Existing ITAC Charter to a certificate of incorporation appropriate for a privately-owned corporation, all as described in “Proposal No. 2. The ITAC Charter Proposal.”

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“Special Meeting” means the Special Meeting of the stockholders of ITAC, to be held virtually on , 2021 at . Eastern time, accessible at or at such other time, on such other date and at such other place to which the meeting may be adjourned or postponed.

“Sponsor” means Industrial Tech Partners, LLC, a Delaware limited liability company.

“Sponsor Shares” means 1,905,900 shares of ITAC Class B Common Stock, which will become the right to receive 1,905,900 Arbe Ordinary Shares pursuant to the Business Combination Agreement.

“Transaction” or “Transactions” means the transactions contemplated by the Business Combination Agreement and the PIPE Subscription Agreements to occur at or immediately prior to the Closing, including the Recapitalization and the Merger.

“Transaction Expenses” means all fees and expenses of any of Arbe or ITAC incurred or payable as of the Closing and not paid prior to the Closing in connection with the consummation of the Transactions, including, without limitation,

5

any amounts payable to professionals (including investment bankers, brokers, finders, attorneys, accountants and other consultants and advisors) retained by or on behalf of ITAC or Arbe, including any all deferred expenses (including fees and commissions payable to underwriter of ITAC’s IPO).

“Trust Account” means the trust account that holds the proceeds of the IPO and of the concurrent sale of the ITAC Private Warrants.

“Trust Agreement” means the investment management trust agreement effective September 11, 2020, between ITAC and Continental Stock Transfer & Trust Company, LLC.

“U.S. dollar,” “USD,” “US$” and “$” mean the legal currency of the United States.

“U.S. GAAP” means generally accepted accounting principles in the United States.

“U.S.” means the United States of America.

“Units” means Units issued in the IPO, each consisting of one share of ITAC Class A Common Stock and one Public Warrant.

“Voting Agreements” means the agreements pursuant to which certain holders of Arbe Preferred Shares and/or Arbe Ordinary Shares agreed to vote their shares of Arbe in favor of the Merger.

“VWAP” means, for any security as of any date(s), the dollar volume-weighted average price for such security on the principal securities exchange or securities market on which such security is then traded during the period beginning at 9:30:01 a.m., New York time, and ending at 4:00:00 p.m., New York time, as reported by Bloomberg through its “HP” function (set to weighted average) or, if the foregoing does not apply, the dollar volume-weighted average price of such security in the over-the-counter market on the electronic bulletin board for such security during the period beginning at 9:30:01 a.m., New York time, and ending at 4:00:00 p.m., New York time, as reported by Bloomberg, or, if no dollar volume-weighted average price is reported for such security by Bloomberg for such hours, the average of the highest closing bid price and the lowest closing ask price of any of the market makers for such security as reported by OTC Markets Group Inc. If the VWAP cannot be calculated for such security on such date(s) on any of the foregoing bases, the VWAP of such security on such date(s) shall be the fair market value as determined reasonably and in good faith by a majority of the disinterested independent directors of the board of directors (or equivalent governing body) of Arbe. All such determinations will be appropriately adjusted for any stock dividend, stock split, stock combination, recapitalization or other similar transaction during such period.

“Warrant Agreement” means that certain warrant agreement, dated as of September 8, 2020, between ITAC and Continental Stock Transfer & Trust Company, LLC.

6

SUMMARY OF THE MATERIAL TERMS OF THE MERGER

The descriptions below of the material terms of the Merger are intended to be summaries of such terms. Such descriptions do not purport to be complete and are qualified in their entirety by reference to the terms of the Business Combination Agreement, which is filed as an exhibit to the registration statement of which this proxy statement/prospectus is a part.

The parties to the Business Combination Agreement are Arbe, Merger Sub and ITAC. Pursuant to the Business Combination Agreement:

i. Pursuant to the Recapitalization, prior to the Effective Time but contingent upon the completion of the Merger, (a) each Exercising Arbe Warrant will be exercised to purchase Arbe Ordinary Shares or Arbe Preferred Shares in accordance with the terms of Exercising Arbe Warrants, (b) immediately following such exercise by the holders of Exercising Arbe Warrants, each outstanding Arbe Preferred Share shall be converted into Arbe Ordinary Shares in accordance with the Arbe Existing Articles and (c) Arbe will effect a recapitalization of the Arbe Ordinary Shares so that the holders of the Arbe Ordinary Shares (and options and warrants to acquire Arbe Ordinary Shares that are not converted to Arbe Ordinary Shares in the Recapitalization) will have shares (or the right to acquire shares, as applicable) valued at $10.00 per share having a total value of $525,000,000, plus the amount of any ITAC transaction expenses (other than expenses related to the PIPE Investment) in excess of $7,000,000, on a fully diluted basis (the ratio at which Company Ordinary Shares are recapitalized being referred to herein as the Conversion Ratio); and (d) with respect to outstanding options and warrants to purchase Arbe Ordinary Shares, the number of Arbe Ordinary Shares issuable upon exercise of such security will be multiplied by the Conversion Ratio and the exercise price of such security will be multiplied by the Conversion Ratio. The Business Combination Agreement does not provide for any purchase price adjustments (other with respect to ITAC transaction expenses above $7,000,000, as described above, for which there is no post-closing adjustment). No fractional Arbe Ordinary Shares shall be issued to holders of Arbe Ordinary Shares, and any fractional shares will be rounded to the next higher integral number of Arbe Ordinary Shares.

ii. Immediately prior to the Effective Time, but after the Recapitalization, subject to the next sentence, the PIPE Investors will purchase 10,000,000 shares of ITAC Class A Common Stock at a purchase price of $10.00 per share, for a total purchase price of $100,000,000 pursuant to the PIPE Subscription Agreements. Notwithstanding the forgoing, pursuant to the PIPE Subscription Agreements, Arbe has the right to issue to the PIPE Investors a total of 10,000,000 Arbe Ordinary Shares after the completion of the Recapitalization, in which event ITAC will no longer have an obligation to sell ITAC Class A Common Stock to the PIPE Investors and the PIPE Investors shall have no right to purchase ITAC Class A Common Stock from ITAC. For the avoidance of doubt, the PIPE Investors shall not participate in the Recapitalization.

iii. Following the consummation of the Recapitalization, Merger Sub will, at the Effective Time, be merged with and into ITAC, which will continue as a wholly-owned subsidiary of Arbe, and in connection therewith, (a) each share of ITAC Common Stock issued and outstanding immediately prior to the Effective Time, including shares of ITAC Class A Stock, if any, issued in a PIPE Investment to be consummated immediately prior to the Effective Time, be cancelled, in exchange for the right of the holder thereof to receive an equal number of Arbe Ordinary Shares, and (b) each ITAC Warrant outstanding immediately prior to the Effective Time will be exchanged for the right to receive an Arbe Warrant to purchase the same number of Arbe Ordinary Shares at the same exercise price during the same exercise period as the ITAC Warrant being exchanged.

iv. The Existing ITAC Charter shall be amended and restated substantially in the form of the Restated ITAC Charter, and each issued and outstanding share of common stock, of Merger Sub will become and be converted into the right to receive one share of common stock, par value $0.01 per share, of ITAC, with the result that the Surviving Company will become a direct, wholly-owned subsidiary of Arbe.

v. As a result of the Recapitalization, each Continuing Arbe Warrant and each Outstanding Arbe Option will become a warrant or an option to purchase such number of Arbe Ordinary Shares, in each instance determined by (i) multiplying the number of Arbe Ordinary Shares issuable upon such exercise of such security by the Conversion Ratio and (ii) dividing the exercise price of such security by the Conversion Ratio. All fractional Arbe Ordinary Shares will be rounded to the next higher integral number of Arbe Ordinary Shares, and the adjusted purchase price or exercise price will be computed to two decimal places.

7

Upon consummation of the Merger, Arbe will become a publicly traded company. Arbe intends to apply for listing of the Arbe Ordinary Shares and Arbe Warrants on Nasdaq under the proposed symbols “ARBE” and “ARBEW,” respectively, to be effective at the consummation of the Merger. It is a condition of the consummation of the Merger that the Arbe Ordinary Shares are approved for listing on Nasdaq (subject only to official notice of issuance thereof). While trading on Nasdaq is expected to begin on the first business day following the date of completion of the Merger, there can be no assurance that Arbe’s securities will be listed on Nasdaq or that a viable and active trading market in the securities will develop following the consummation of the Merger

Upon the consummation of the Merger, the number of directors of Arbe will be set at seven persons, with the initial post-Closing directors being those persons named under “Management of Arbe Following the Merger.” The Business Combination Agreement provides that these directors will be selected as follows: (i) four directors will be designated by Arbe, at least two of whom will be independent directors, (ii) one director designated by ITAC, and (iii) two independent directors mutually agreed on by Arbe and ITAC. The independent directors will meet the Nasdaq definition of independent director. Upon completion of the Merger, the current officers of Arbe will remain officers of Arbe, holding equivalent positions to those held by them with Arbe prior to the Merger. See the section entitled “Management of Arbe Following the Merger.”

Each party agreed in the Business Combination Agreement to use its commercially reasonable efforts to effect the Closing. The Business Combination Agreement also contains certain customary covenants by each of the parties relating to their respective business and operations during the period between the signing of the Business Combination Agreement and the earlier of (x) the Closing or (y) the earlier termination of the Business Combination Agreement in accordance with its terms (the “Interim Period”), in each instance, and as more thoroughly described in the Business Combination Agreement, including those relating to: (i) the provision of access to their properties, books and personnel; (ii) the operation of their respective businesses in the ordinary course of business; (iii) the provision of financial statements by Arbe to ITAC; (iv) ITAC’s public filings; (v) no insider trading; (vi) notifications of certain breaches, consent requirements or other matters; (vii) efforts to consummate the Closing; (viii) further assurances; (ix) public announcements; and (x) confidentiality. Each party also agreed, during the Interim Period, not to solicit or enter into any inquiry, proposal or offer, or any indication of interest in making an offer or proposal for an alternative competing transaction, to notify the others as promptly as practicable in writing of the receipt of any inquiries, proposals or offers, requests for information or requests relating to an alternative competing transaction or any requests for non-public information relating to such transaction, and to keep the other party informed of the status of any such inquiries, proposals, offers or requests for information. The Business Combination Agreement also contains certain customary post-Closing covenants regarding (a) maintenance of books and records; (b) indemnification of directors and officers and the purchase of tail directors’ and officers’ liability insurance; and (c) use of trust account proceeds.

The Business Combination Agreement contains conditions to Closing customary for a transaction of this nature, including the following mutual conditions of the parties (unless waived to the extent legally permissible): (i) approval of the shareholders of ITAC and Arbe; (ii) approvals of any required governmental authorities and completion of any antitrust expiration periods; (iii) receipt of specified third party consents; (iv) no law or order preventing the Transaction; (v) the Registration Statement having been declared effective by the SEC; (vi) no material uncured breach by the other party; (vii) no occurrence of a Material Adverse Effect with respect to the other party; (viii) the satisfaction of the $5,000,001 minimum net tangible asset test by Arbe or ITAC; (ix) approval of Arbe’s Nasdaq listing application; and (x) reconstitution of the Post-Closing Board as contemplated under the Business Combination Agreement.

In addition, unless waived by Arbe, the obligations of Arbe and Merger Sub to consummate the Merger are subject to the satisfaction of the following additional Closing conditions, in addition to the delivery by ITAC of customary certificates and other Closing deliverables: (i) the representations and warranties of ITAC being true and correct as of the date of the Business Combination Agreement and as of the Closing (subject to certain materiality qualifiers); (ii) ITAC having performed in all material respects its obligations and complied in all material respects with its covenants and Agreements under the Business Combination Agreement required to be performed or complied with by it on or prior to the date of the Closing; (iii) absence of any Material Adverse Effect with respect to ITAC since the date of the Business Combination Agreement which is continuing and uncured; (iv) the execution of the Founder Lock-Up Agreement; and (v) at the Closing, ITAC will have at least $100,000,000 in cash and cash equivalents, including funds remaining in the trust account (after giving effect to the completion and payment of any redemptions) and the proceeds of any PIPE Investment (including any PIPE Investment directly into Arbe, as described above), prior to paying any of ITAC’s expenses and liabilities due at the Closing.

8

Unless waived by ITAC, the obligations of ITAC to consummate the Merger are subject to the satisfaction of the following additional Closing conditions, in addition to the delivery by Arbe and Merger Sub of customary certificates and other Closing deliverables: (i) the representations and warranties of Arbe and Merger Sub being true and correct as of the date of the Business Combination Agreement and as of the Closing (subject to certain materiality qualifiers); (ii) Arbe and Merger Sub having performed in all material respects their respective obligations and complied in all material respects with their respective covenants and Agreements under the Business Combination Agreement required to be performed or complied with by them on or prior to the date of the Closing; (iii) absence of any Material Adverse Effect with respect to Arbe or Merger Sub since the date of the Business Combination Agreement which is continuing and uncured; (iv) the Lock-Up Agreements (as described below) being in full force and effect as of the Closing; and (v) non-competition Agreements (in a form to be mutually agreed prior to Closing) having been executed and delivered by certain executive officers of Arbe and be in full force and effect as of the Closing.

The Business Combination Agreement may be terminated under certain customary and limited circumstances at any time prior to the Closing, including: (i) by mutual written consent of ITAC and Arbe; (ii) by either ITAC or Arbe if any of the conditions to Closing have not been satisfied or waived by August 31, 2021; (iii) by either ITAC or Arbe if a governmental authority of competent jurisdiction has issued an order or taken any other action permanently restraining, enjoining or otherwise prohibiting the Transaction, and such order or other action has become final and non-appealable; (iv) by either ITAC or Arbe in the event of the other party’s uncured breach, if such breach would result in the failure of a closing condition (and so long as the terminating party is not also in breach under the Business Combination Agreement); (v) by ITAC if there has been a Material Adverse Effect on Arbe and its subsidiaries on a consolidated basis following the date of the Business Combination Agreement that is uncured and continuing; (vi) by Arbe if there has been a Material Adverse Effect on ITAC following the date of the Business Combination Agreement that is uncured and continuing; and (vii) by either ITAC or Arbe if Arbe holds a special meeting of its shareholders to approve the Business Combination Agreement and the Transaction and such approval is not obtained.

Pursuant to the Business Combination Agreement, Arbe entered into a Founder Registration Rights Amendment pursuant to which Arbe agreed to assume ITAC’s obligations under the registration rights agreement signed by ITAC and the Sponsor at the time of ITAC’s initial public offering.

Pursuant to the Business Combination Agreement, Arbe agreed to file a registration statement on Form F-1 covering (i) sale by the holders of the Arbe Ordinary Shares which are outstanding immediately following the Recapitalization (but prior to the PIPE Investment and the issuance of Arbe Ordinary Shares and Arbe Warrants to the holders of ITAC Common Stock and ITAC Warrants) and (ii) the issuance of Arbe Ordinary Shares upon exercise of Continuing Warrants. Certain Arbe significant shareholders and insiders have executed a lock-up agreement pursuant to which each of them agreed during the one-year period subsequent to the Closing not to sell any of their Arbe Ordinary Shares, subject to release if and to the extent certain stock price levels are reached. These lock-up agreements apply to shares registered pursuant to a registration statement on Form F-1.

Pursuant to the PIPE Subscription Agreements, Arbe also agreed to file a registration statement covering the Arbe Ordinary Shares issued in the PIPE Investment (or any ITAC Shares issues in the PIPE Investment and converted into Arbe Ordinary Shares in connection with the consummation of the Merger).

9

QUESTIONS AND ANSWERS ABOUT THE PROPOSALS

|

Q. Why am I receiving this proxy statement/prospectus? |

A. ITAC and Arbe have agreed to pursue the Merger under and in accordance with the terms of the Business Combination Agreement that is described in this proxy statement/prospectus. A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A and ITAC encourages its stockholders to read it in its entirety. ITAC’s stockholders are being asked to consider and vote upon a proposal to approve the Business Combination Agreement and certain other related matters, which, among other things, provides for Merger Sub to be merged with and into ITAC with ITAC being the surviving corporation in the Merger and becoming a wholly-owned subsidiary of Arbe, and the holders of ITAC Common Stock and ITAC Warrants becoming holders of Arbe Ordinary Shares and Arbe Warrants, respectively. See “Proposal No. 1 — The Business Combination Proposal” and “Description of the Business Combination Agreement.” |

|

|

Q. In addition to the Business Combination Proposal, what is being voted on at the Special Meeting? |

A. In addition to the Business Combination Proposal, ITAC’s stockholders are being asked to vote to adopt the Restated ITAC Charter, which changes the name of ITAC to Autobot HoldCo, Inc., changes the authorized capital stock to 100 shares of common stock and otherwise restates the Existing ITAC Charter to a certificate of incorporation appropriate for a privately-owned corporation. Following the consummation of the Merger, ITAC will become a wholly-owned subsidiary of Arbe. See the “Proposal No. 2 — ITAC Charter Proposal.” |

|

|

The ITAC stockholders may also be asked to consider and vote upon a proposal to adjourn the meeting to a later date or dates to permit further solicitation and voting of proxies if, based upon the tabulated vote at the time of the Special Meeting, ITAC would not have been authorized to consummate the Merger. See the section entitled “Proposal No. 3 — The Adjournment Proposal.” |

||

|

ITAC will hold the Special Meeting of its stockholders to consider and vote upon these proposals. This proxy statement/prospectus contains important information about the proposed Merger and the other matters to be acted upon at the Special Meeting. Stockholders should read it, including the documentation annexed hereto, carefully. |

||

|

The vote of stockholders is important. Stockholders are encouraged to submit their completed proxy card as soon as possible after carefully reviewing this proxy statement/prospectus. |

||

|

Q. Why is ITAC proposing the Merger? |

A. ITAC was organized to effect a merger, capital stock exchange, asset acquisition or other business combination similar to the Merger with one or more businesses or entities. |

|

|

ITAC completed its IPO of 7,500,000 Units on September 11, 2020, with each Unit consisting of one share of ITAC Class A Common Stock and one ITAC Public Warrant, concurrently with a private placement of 3,075,000 ITAC Private Warrants for $3,075,000. Each ITAC Warrant (both the Public Warrants and the Private Warrants) entitles the holder to purchase one share of ITAC Class A Common Stock at a price of $11.50. On October 13, 2020, the Company completed the sale of an additional 123,600 Units that were subject to the underwriters’ over-allotment option at $10.00 per Unit, generating gross proceeds of $1,236,000. Following the closing of the over-allotment option, an aggregate amount of $76,998,360 has been placed in the Trust Account established in connection with the IPO. Since the IPO, ITAC’s activity has been limited to the evaluation of Merger candidates. |

10

|

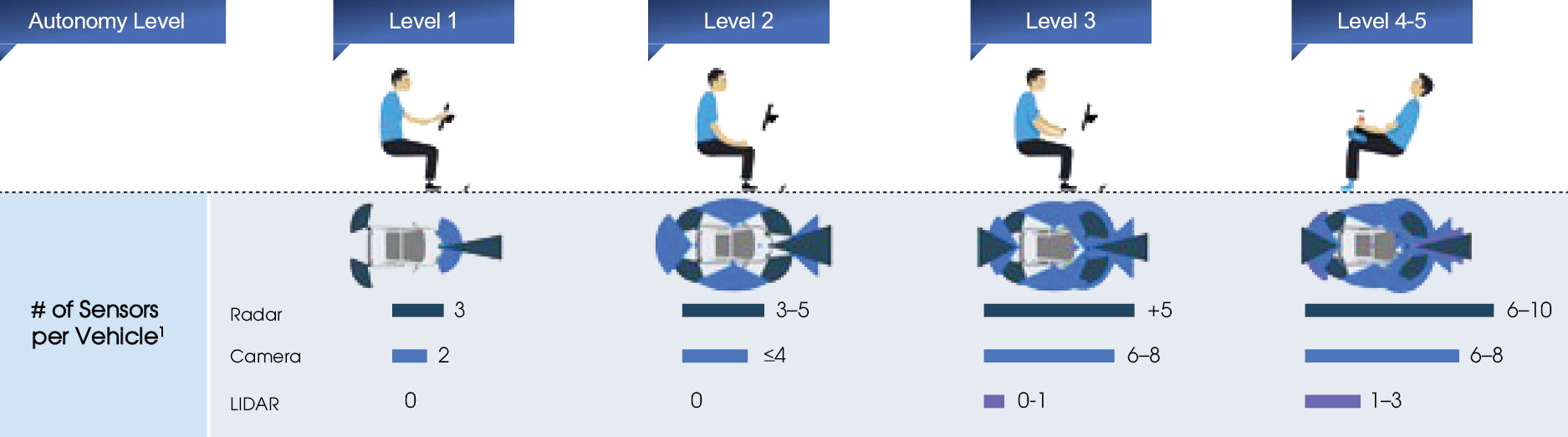

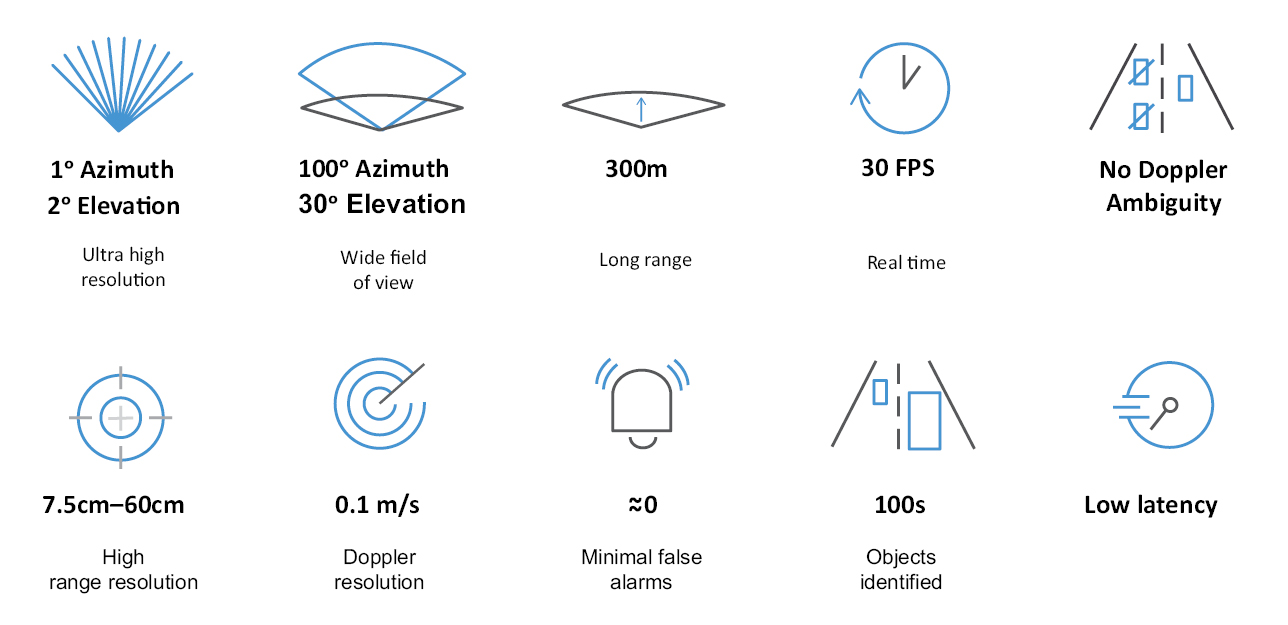

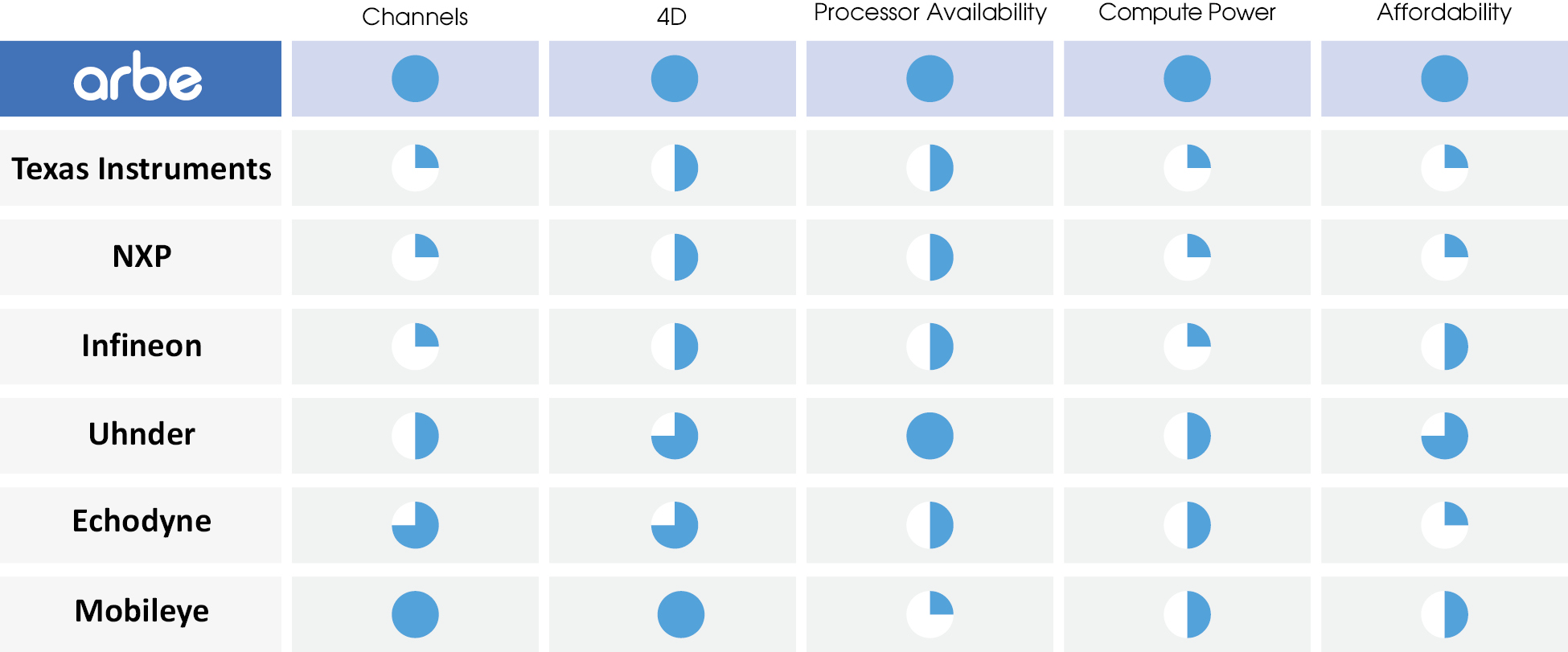

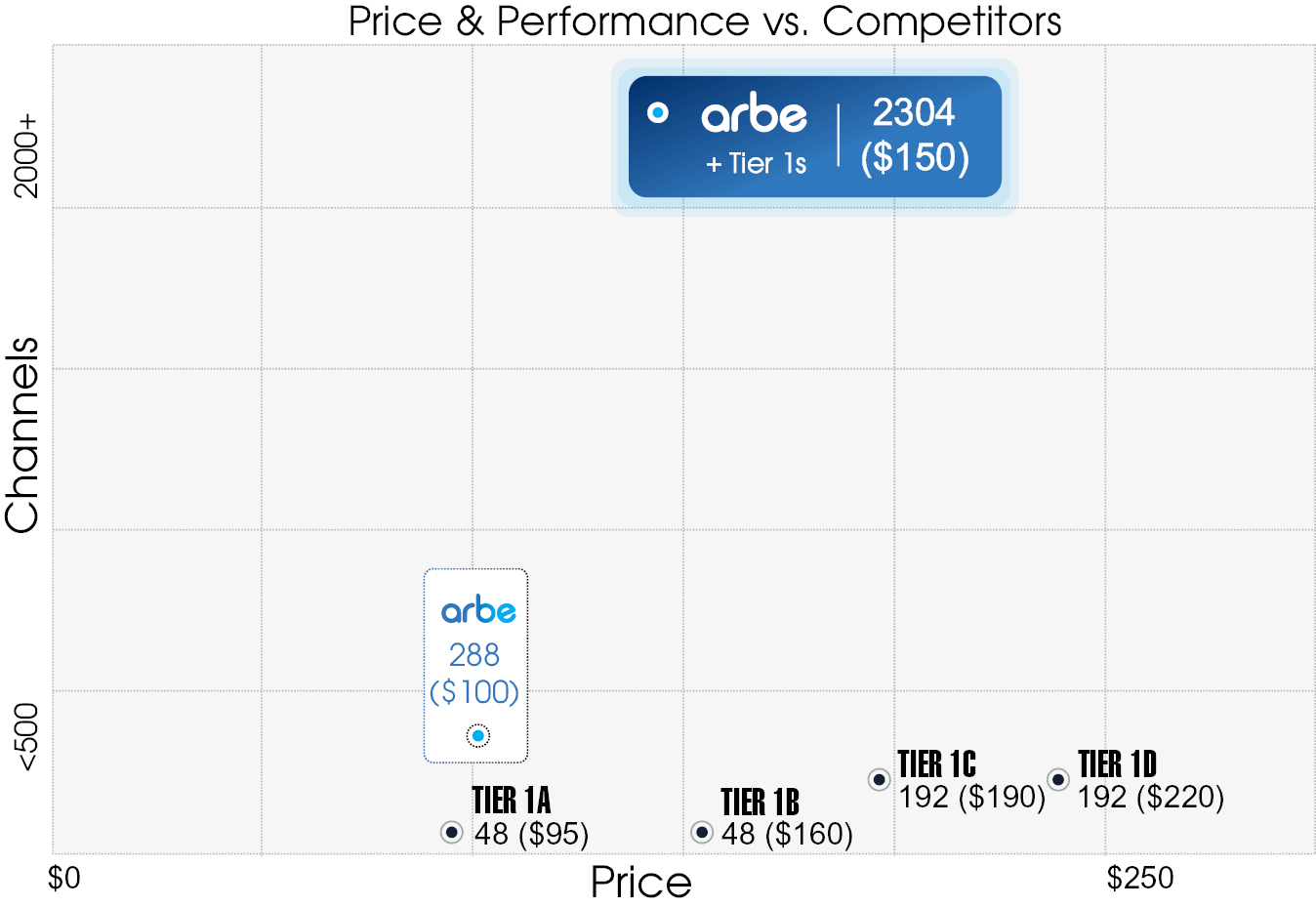

Arbe is a provider of 4D Imaging Radar solutions, and is leading a radar revolution, enabling truly safe driver-assist systems today while paving the way for fully autonomous driving. Arbe is empowering automakers, tier-1 companies, and enabling autonomous ground vehicles, commercial and industrial vehicles, and a wide array of safety applications with next-generation sensing and paradigm-changing perception. Arbe’s Imaging Radar offers an order of magnitude higher resolution than any other competing radar solution in the market, and is an essential sensor for L2+ and higher levels of autonomy. Arbe’s solution includes an RF chipset with the largest channel array in the industry, a groundbreaking radar processor chip, and artificial intelligence (AI)-based post-processing. Founded in 2015, Arbe has offices in Israel and the United States. Based on ITAC’s due diligence investigations of Arbe and the industry in which it operates, including the financial and other information provided by Arbe in the course of their negotiations, ITAC believes that Arbe has an appealing growth profile and that the proposed Merger presents a compelling valuation. As a result, ITAC believes that the proposed Merger with Arbe will provide ITAC stockholders with an opportunity to participate in a company with significant growth potential. See the section entitled “Proposal No. 1 — The Business Combination Proposal — The ITAC Board of Directors’ Reasons for the Merger.” |

||

|

Q. What will happen to ITAC’s securities upon consummation of the Merger? |

A. Each outstanding ITAC Unit will be separated into its components — the ITAC Common Stock and the ITAC Warrants — and the ITAC Units will cease to trade. The ITAC Units, ITAC Class A Stock and the ITAC Warrants are currently listed on Nasdaq under the symbols “ITACU,” “ITAC” and “ITACW,” respectively. ITAC’s securities will cease trading following the consummation of the Merger. Arbe intends to apply for listing of the Arbe Ordinary Shares and Arbe Warrants on Nasdaq under the proposed symbols “ARBE” and “ARBEW,” respectively, to be effective upon consummation of the Merger. While trading on Nasdaq is expected to begin on the first business day following the consummation of the Merger, there can be no assurance that Arbe’s securities will be listed on Nasdaq or that a viable and active trading market will develop. A Nasdaq listing is a condition to Arbe’s obligation to close, so, unless Arbe waives the closing condition, the Merger will not be completed if the Arbe Ordinary Shares are not listed on Nasdaq. See “Risk Factors — Risks Related to the Merger” for more information. |

|

|

Q. What will happen in the Merger? |

A. Subject to the terms and conditions set forth in the Business Combination Agreement, at the Closing, Merger Sub will merge with and into ITAC, with ITAC surviving as a wholly-owned subsidiary of Arbe. Each share of ITAC Common Stock will become and be converted into the right to receive one Arbe Ordinary Share and each ITAC Warrant will become and be converted into the right to receive an Arbe Warrant to purchase the same number of Arbe Ordinary Shares at the same exercise price per share as the ITAC Warrant, which is $11.50 per share. |

|

|

More specifically, immediately following Closing, assuming the “No Redemption Scenario”: • All of the outstanding shares of ITAC Common Stock, consisting of (i) 7,774,836 shares of ITAC Class A Common Stock, of which 7,623,600 are held by the Public Stockholders, (ii) 1,905,900 shares ITAC Class B Common Stock held by the Sponsor, and (iii) 10,000,000 shares of ITAC Class A Common to be held by the PIPE Investors (unless Arbe elects to issue 10,000,000 Arbe Ordinary Shares to the PIPE Investors directly) will be converted into the right receive a total of 19,680,736 Arbe Ordinary Shares. |

11

|

• All of the outstanding ITAC Warrants, consisting of (i) 7,623,600 ITAC Public Warrants held by ITAC’s Public Stockholders and (ii) 3,112,080 ITAC Private Warrants, will become and be converted into a total of 10,735,680 Arbe Warrants. In addition, the Sponsor may, but is not obligated to, lend funds to ITAC as may be required for working capital, in connection with the business combination. Such working capital loans would be convertible into ITAC Private Warrants at a price of $1.00 per warrant (which, for example, would result in the holders being issued 1,500,000 ITAC warrants if $1,500,000 of notes were converted. ITAC has issued its $250,000 non-interest bearing promissory note to the Sponsor and the Sponsor has funded $100,000 under the note as of the date of the proxy statement/prospectus. This note is convertible at the election of the holder, into one ITAC Private Warrant for each dollar of the outstanding principal amount of the note that is converted. To the extent this note is converted into ITAC Private Warrants, the number of Arbe Warrants to be issued will be increased. The Sponsor has advised ITAC that it does not intend to convert the convertible note. In connection with ITAC’s initial public offering, ITAC issued to Maxim an option to purchase up to a total of 203,296 units (each consisting of one share of ITAC Common Stock and one redeemable ITAC public warrant to purchase one share of ITAC Common Stock at $11.50 per unit, commencing on the later of (i) the consummation of a business combination by ITAC and (ii) six months from September 11, 2020. Pursuant to the Merger, this unit purchase option will become an option to purchase 203,296 units, each unit consisting of one Arbe Ordinary Shares and one Arbe Warrant. • After the Recapitalization, at the Effective Time, the Arbe security holders will hold a total of 48,275,832 Arbe Ordinary Shares, Arbe Continuing Warrants to purchase 288,076 Arbe Ordinary Shares and Arbe Continuing Options to purchase a total of 3,996,092 Arbe Ordinary Shares. Accordingly, after the consummation of the Merger and the issuance of the PIPE Shares, there will be a total of (i) 67,956,568 Arbe Ordinary Shares outstanding, and (ii) an additional 10,932,796 Arbe Ordinary Shares reserved issuance upon exercise of the (x) the Arbe Warrants issuable in exchange for the 7,623,600 ITAC Public Warrants and 3,105,900 ITAC Private Warrants, (y) 203,296 Arbe Ordinary Shares issuable upon the exercise of the Underwriter’s unit purchase option and 203,296 Arbe Ordinary Shares issuable upon exercise of the Arbe Warrants issuable upon exercise of the underwriter’s unit purchase option, and (z) 4,224,168 shares issuable upon exercise of the Arbe Continuing Warrants (228,076 shares) and the Outstanding Arbe Options (3,996,092 shares). In addition, ITAC Private Warrants may be issued upon conversion of the ITAC convertible promissory note issued to the Sponsor. However, the Sponsor has advised ITAC that it does not intend to convert the convertible note. |

||

|

Q. Are the proposals conditioned on one another? |

Yes. The Merger is conditioned on the approval of Restated Charter Proposal and the Restated Charter Proposal is conditioned on the approval of the Business Combination Proposal. The Adjournment Proposal is not conditioned upon the approval of any other proposal. |

|

|

Q. What will be the relative equity stakes of ITAC’s public stockholders, the Sponsor, the PIPE Investors and Arbe’s existing shareholders in Arbe upon completion of the Merger? |

A. Upon consummation of the Merger, Arbe will become a public company and ITAC will become a wholly-owned subsidiary of Arbe. In connection therewith, the former security holders of ITAC and the PIPE Investors will all become security holders of Arbe. |

12

|

Upon consummation of the Merger, assuming the No Redemption Scenario and after giving effect to the Recapitalization, the post-Closing share ownership of Arbe Ordinary Shares would be as follows: |

|

|

Arbe Ordinary |

||||||

|

ITAC public stockholders |

7,623,600 |

(11.22 |

)% |

||||

|

Sponsor(2) |

1,905,900 |

(2.80 |

)% |

||||

|

Maxim |

151,236 |

(0.22 |

)% |

||||

|

PIPE Investors |

10,000,000 |

(14.72 |

)% |

||||

|

Existing Arbe shareholders(3) |

48,275,832 |

(71.04 |

)% |

||||

|

Total |

67,956,568 |

(100.00 |

)% |

||||

|

_________ (1) Excludes all 10,932,796 ITAC Warrants, including ITAC Warrants issuable upon exercise of Maxim’s unit purchase option. (2) Excludes Arbe Ordinary Shares issuable upon exercise of ITAC Private Warrants. (3) Excludes Arbe Continuing Warrants and Outstanding Arbe Options to purchase a total of 4,224,168 Arbe Ordinary Shares. |

|

The number of Arbe Ordinary Shares to be held by the existing Arbe Shareholders reflects the Recapitalization and is subject to increase in the event that ITAC’s Transaction Expenses (other than expenses relating to the PIPE Investment) exceed $7,000,000. See “The Business Combination Agreement.” Pursuant to the Existing ITAC Charter, in connection with the completion of the Merger, each ITAC Public Stockholder may elect to have its shares redeemed for cash at the applicable redemption price per share calculated in accordance with the Existing ITAC Charter. Payment for such redemptions will come from the Trust Account. To the extent ITAC’s Public Stockholders elect to have their shares redeemed, the consideration to be paid and the relative ownership table described above will be modified accordingly. A final ownership calculation will be disclosed upon Closing of the Merger. |

||

|

Q. What are the U.S. Federal income tax consequences of the Merger to U.S. holders of ITAC Common Stock and/or Public Warrants? |

A. As described more fully under the section entitled “Certain Material U.S. Federal Income Tax Considerations — U.S. Holders — U.S. Federal Income Tax Considerations of the Merger,” the parties to the Merger intend that the Merger qualify as a tax-deferred reorganization within the meaning of Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”) to U.S. Holders (as defined below) of ITAC Common Stock and/or ITAC Warrants. |

|

|